Construction Loan Process

For Real Estate Investors

The construction loan process for real estate investors helps borrowers understand how ground-up construction loans are reviewed, approved, closed, and funded through draw schedules. Direct Private Capital Group, Inc. reviews borrower information, property details, budgets, permits, valuation, liquidity, and exit strategy to help qualified borrowers explore private construction financing options. Terms, approval, funding, and availability are subject to underwriting, collateral review, state eligibility, and lender/investor guidelines.

What This Page Helps Borrowers Understand

A construction loan can be more complex than a standard purchase loan or refinance because the lender is not only reviewing the property as it exists today. The lender also reviews the future project, construction budget, builder experience, permits, timeline, draw schedule, borrower liquidity, and exit strategy.

This page explains what happens before a construction loan is reviewed, approved, closed, and funded. It helps borrowers understand what documents are usually requested, what causes delays, how draw schedules work, and what to prepare before submitting a loan scenario.

A complete construction loan package does not guarantee approval or funding. It can help Direct Private Capital Group, Inc. understand the transaction and review available private lending options based on the borrower, collateral, project plan, state eligibility, and lender/investor guidelines.

Who This Page Is For

This resource is designed for real estate investors, builders, developers, brokers, foreign national investors, commercial property owners, hospitality investors, gas station operators, and business-purpose borrowers seeking private construction financing in the United States.

It may be useful for ground-up residential investment construction, small multifamily construction, commercial property construction, mixed-use development, hotel or hospitality projects, gas station or convenience store construction, investor-built rental properties, spec homes, and business-purpose redevelopment projects.

Business-purpose financing note: Direct Private Capital Group, Inc. reviews business-purpose real estate financing scenarios. This page does not apply to consumer-purpose residential mortgage loans, owner-occupied consumer mortgages, or personal-purpose borrowing.

What Lenders Usually Review

Private construction loan review usually considers the borrower profile, land or property collateral, requested loan amount, construction budget, permit status, loan-to-cost, loan-to-value, completed value, borrower liquidity, builder experience, title condition, insurance, draw schedule, and exit strategy. Requirements vary by property, state, borrower profile, project type, and lender/investor guidelines.

What Can Delay Review

Common delays include missing plans, unclear permit status, incomplete construction budgets, no contingency reserve, title issues, missing valuation support, no builder information, incomplete entity documents, unclear draw schedule, insurance delays, weak exit strategy, or a project that does not fit state or investor guidelines. Complete information can help the file be reviewed more clearly, but does not guarantee approval or funding.

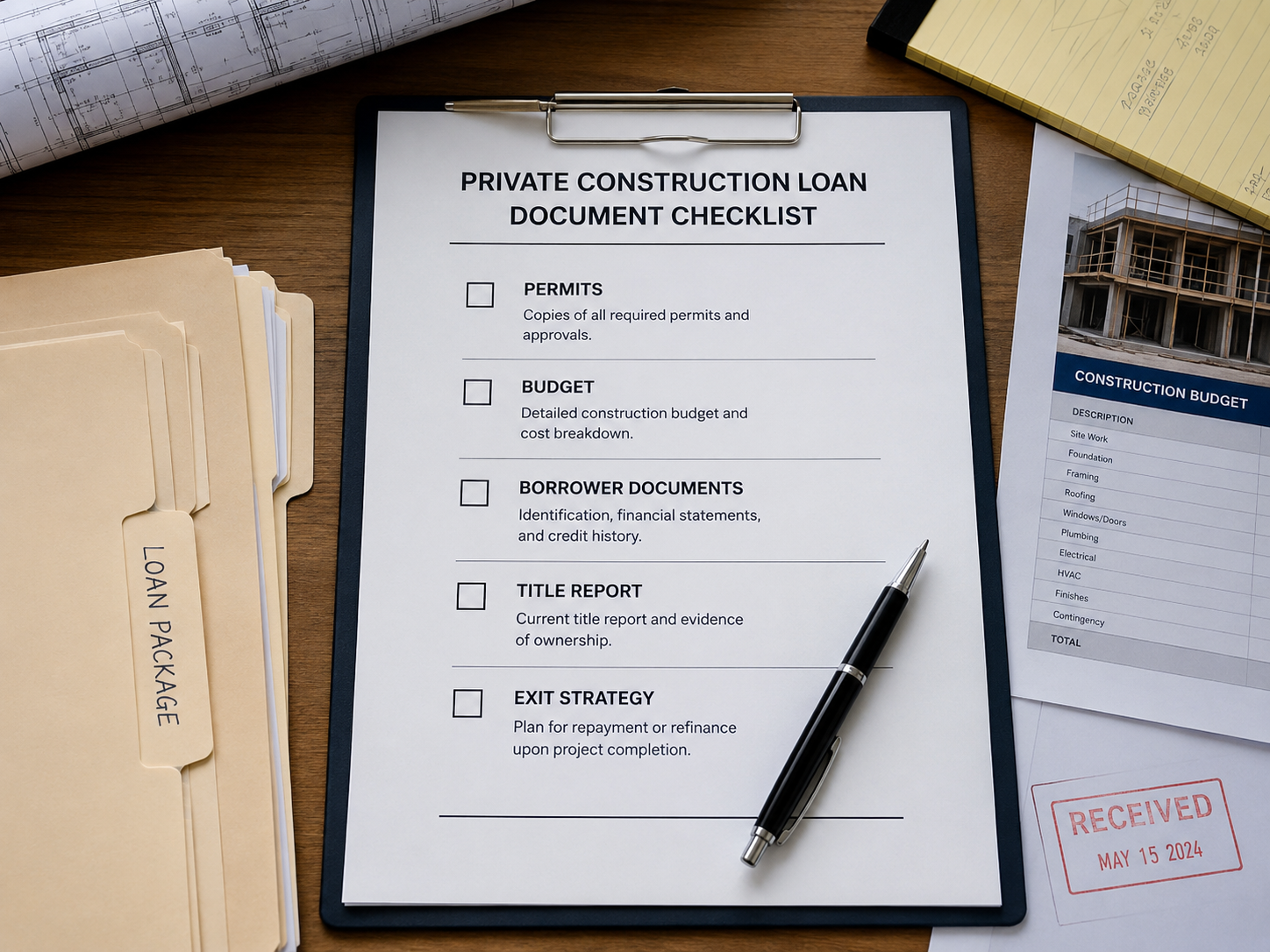

CONSTRUCTION LOAN DOCUMENTS COMMONLY REQUESTED

BORROWER INFORMATION

- Borrower legal name, contact information, and borrowing entity

- Entity documents, ownership structure, EIN, and authorization to borrow

- Government ID, credit authorization, liquidity, and proof of funds

- Builder, developer, or investor experience and completed project history

PROPERTY INFORMATION

- Property address, property type, land value, site photos, and current condition

- Purchase contract, payoff statement, title report, insurance, and valuation support

- Plans, site plan, zoning, permit status, utilities, and entitlement details

- Environmental, survey, appraisal, BPO, or property-specific reports when applicable

PROJECT SCENARIO

- Requested loan amount, lien position, land payoff or purchase price, and use of funds

- Hard cost budget, soft cost budget, contingency reserve, and construction timeline

- Loan-to-cost, loan-to-value, completed value, and borrower cash contribution

- Draw schedule, inspection process, exit strategy, and repayment plan

Submission note: Borrowers and brokers should confirm whether borrower documents, property records, valuation support, construction budget, plans, permit status, title information, insurance details, and exit strategy are available. Public resources from the Consumer Financial Protection Bureau and the U.S. Small Business Administration may provide general finance and business education. Construction loan review remains subject to underwriting, collateral review, state eligibility, and lender/investor guidelines.

CONSTRUCTION LOAN REVIEW PROCESS

A clear construction loan submission helps Direct Private Capital Group, Inc. review whether available private lending options may fit the borrower, collateral, budget, permits, completed value, draw schedule, exit strategy, state eligibility, and lender/investor guidelines.

FROM SCENARIO SUBMISSION TO DRAW FUNDING CONSIDERATION

Preliminary review of borrower, collateral, construction budget, permit status, leverage, liquidity, and exit strategy

Submit requested documents for underwriting, collateral review, valuation review, title review, and budget review

Closing conditions, title, insurance, valuation, draw schedule, and funding consideration

Why the Construction Loan Process Matters for Real Estate Investors

The construction loan process matters because incomplete information can delay review, create uncertainty, or prevent a lender from issuing accurate preliminary terms. A strong construction loan submission helps investors explain the property, the project, the budget, the repayment plan, and why the loan request makes sense.

Private construction lenders usually want to understand who the borrower is, what property secures the loan, what is being built, how much the project will cost, what permits or approvals are in place, how funds will be released, and how the loan will be repaid.

A complete file does not guarantee approval or funding. It can make the review more efficient and help the lender or investor understand the transaction more clearly.

What the Construction Loan Process Does and Does Not Mean

The construction loan process may include review for ground-up construction loans, private construction loans, bridge-to-construction scenarios, commercial real estate construction financing, hotel construction financing, gas station development financing, and investor-built rental properties. It does not mean every borrower, property, or construction project will qualify.

It May Be Used For

- Ground-up construction loans

- Private construction loans

- Investor-built rental properties

- Spec home construction

- Small multifamily construction

- Commercial property construction

- Hotel or hospitality construction

- Gas station and convenience store development

- Business-purpose redevelopment projects

It Does Not Mean

- No underwriting

- No collateral review

- No title review

- No valuation review

- No borrower review

- No permit or budget review

- Guaranteed approval

- Guaranteed funding

- Guaranteed rate or term

- Eligibility for every project in every state

Key Construction Loan Requirements, Documents, and Review Factors

Borrower Information Usually Reviewed

- Borrower name and contact information

- Borrowing entity name and entity documents

- Government-issued identification

- Credit profile, when required

- Real estate owned schedule

- Borrower liquidity and proof of funds

- Builder, developer, or construction experience

- Personal financial statement, when required

- Foreign national documentation, when applicable

Property Information Usually Reviewed

- Property address, property type, land size, building size, and current use

- Purchase contract for acquisition loans or payoff statement for refinance loans

- Property photos, appraisal, BPO, comparable sales, or other valuation support

- Title report, insurance information, and property tax details

- Zoning, permits, site plan, approved plans, utility availability, and entitlement status

- Environmental reports, survey, or special property documents when relevant

- Current condition, site access, and construction readiness

Loan Scenario Information Usually Reviewed

- Requested loan amount

- Loan purpose

- Land payoff or purchase price

- Existing debt

- Hard construction costs

- Soft costs

- Contingency reserve

- Construction timeline

- Requested term

- Interest reserve request, if applicable

- Collateral position

- Borrower contribution or cash to close

- Use of proceeds

Exit Strategy or Repayment Plan

The exit strategy explains how the borrower expects to repay the construction loan after the project is completed. Examples may include selling the completed property, refinancing into DSCR financing, refinancing into commercial permanent financing, stabilizing a commercial property and obtaining long-term debt, selling units, or repaying the loan from another documented capital source.

How the Construction Draw Process Usually Works

A construction draw process is the method used to release loan funds as work is completed. Instead of giving all construction funds to the borrower at closing, the lender usually funds construction in stages based on the approved budget and draw schedule.

- Initial closing: The loan closes after underwriting, title, insurance, loan documents, and closing conditions are satisfied.

- Work begins: The borrower or contractor starts the approved construction work.

- Draw request is submitted: The borrower, contractor, or project manager submits invoices, photos, lien waivers, receipts, or other draw support.

- Inspection or verification occurs: The lender may require a third-party inspection or internal review to verify completed work.

- Approved funds are released: If the draw is approved, funds are released according to the loan agreement and draw schedule.

- The process repeats: Draws continue through major milestones until the project is complete.

Draw approvals are not automatic. They may be subject to inspection, budget review, title updates, lien waiver requirements, and lender/investor guidelines.

Loan Review Factors Table

| Review Factor | Why It Matters | What Borrowers Should Prepare |

|---|---|---|

| Borrower experience | Execution risk matters in construction projects | Resume, prior projects, real estate owned schedule |

| Liquidity | Construction projects may require reserves for delays or overruns | Bank statements, proof of funds, financial statement |

| Land or collateral value | Private lenders rely heavily on property review | Appraisal, BPO, comparable sales, property photos |

| Loan-to-cost | Measures the loan amount against total project cost | Purchase price, land payoff, budget, sources and uses |

| Loan-to-value | Measures the loan amount against property value or completed value | As-is value, completed value, appraisal, BPO, comparable sales |

| Construction budget | Shows whether the project cost is realistic | Hard costs, soft costs, contingency, contractor bid |

| Permits and approvals | Missing approvals can delay or prevent funding | Permit status, plans, site plan, zoning information |

| Draw schedule | Helps control risk during construction | Milestone-based draw schedule and inspection plan |

| Title and liens | Confirms ownership, payoff needs, and lien position | Title report, payoff statements, existing debt details |

| Exit strategy | Shows how the loan may be repaid | Sale plan, refinance plan, lease-up plan, or stabilization plan |

Helpful business planning note: Borrowers comparing financing structures may review general resources from the Consumer Financial Protection Bureau, U.S. Small Business Administration, and U.S. Census Bureau. Private construction loan review still depends on the property, collateral, borrower profile, valuation, budget, permit status, loan purpose, state eligibility, and lender/investor guidelines.

Common Reasons a Construction Loan File Gets Delayed

- Missing loan application

- No clear loan amount requested

- Incomplete borrower entity documents

- Missing construction budget

- Budget does not separate hard costs and soft costs

- No contingency reserve

- Missing plans or site plan

- Permit status is unclear

- Zoning or entitlement issues

- Contractor is not identified

- Contractor bid is incomplete

- Title issues or unresolved liens

- Property value support is missing

- Borrower liquidity is not documented

- Exit strategy is weak or unrealistic

- Insurance information is incomplete

- Environmental issues are unresolved

- Draw schedule is not aligned with the budget

- State eligibility or licensing issues need review

How to Prepare Before Submitting a Construction Loan Scenario

Prepare a Short Construction Loan Summary

- Borrower name

- Borrowing entity

- Property address

- Property type

- Loan purpose

- Requested loan amount

- Purchase price or current land value

- Existing payoff, if any

- Total construction budget

- Estimated completed value

- Borrower cash contribution

- Requested loan term

- Exit strategy

Prepare the Construction Package

- Plans

- Site plan

- Construction budget

- Contractor bid

- Contractor license, if applicable

- Construction timeline

- Permit status

- Draw schedule

- Completed value support

- Photos of the site

- Proof of utilities, if available

Prepare the Borrower Package

- Loan application

- IDs

- Credit authorization

- Entity documents

- Bank statements

- Personal financial statement

- Experience summary

- Real estate owned schedule

- Proof of funds or liquidity

- Foreign national documents, if applicable

Related Financing Topics

The construction loan process may connect to ground-up construction loans, required documents, the loan process, FAQ, contact page, and apply now.

What This Page Does Not Guarantee

This page is educational. It does not guarantee loan approval, funding, terms, rates, closing timelines, search rankings, AI recommendations, or loan availability. Direct Private Capital Group, Inc. does not represent that every borrower, property, or construction loan request will qualify for financing.

Loan availability may depend on borrower qualifications, credit profile, liquidity, collateral value, completed value, construction budget, permit status, property condition, property type, loan purpose, loan amount, lien position, title condition, insurance availability, state eligibility, exit strategy, lender and investor guidelines, and applicable federal and state laws.

Submit Your Construction Loan Scenario

If you are preparing a ground-up construction project, redevelopment, or business-purpose real estate construction loan request, submit the project details for review. Direct Private Capital Group, Inc. reviews construction loan scenarios across eligible U.S. markets.

Submit your loan scenario today and let Direct Private Capital Group, Inc. review available private lending options for your project.

Compliance Disclaimer

Direct Private Capital Group, Inc. provides business-purpose real estate financing information. This page is for informational purposes only and is not a commitment to lend, loan approval, or guarantee of terms. All loans are subject to underwriting, borrower qualification, collateral review, valuation, state eligibility, lender/investor guidelines, and applicable federal and state laws.

Helpful Finance and Construction Resources

Borrowers may review general public finance and business planning resources from the Consumer Financial Protection Bureau, U.S. Small Business Administration, and U.S. Census Bureau. Construction borrowers should also review local building department and state contractor licensing resources when applicable. Direct Private Capital Group, Inc. provides business-purpose real estate financing information, and this page is not legal, tax, valuation, construction, environmental, or consumer mortgage advice.Frequently Asked Questions About the Construction Loan Process

The construction loan process for real estate investors usually includes loan scenario review, borrower qualification, collateral review, budget analysis, permit review, underwriting, closing, and construction draw funding. Each step is subject to lender/investor guidelines.

Common documents include a loan application, borrower IDs, entity documents, bank statements, credit authorization, construction budget, plans, permit status, title report, valuation support, contractor information, insurance, and exit strategy.

A construction draw process releases funds in stages as work is completed. The borrower usually submits a draw request, supporting invoices, photos, and other documents. The lender may require inspection or verification before releasing funds.

A file may be reviewed before permits are issued, but missing permits can limit available options or delay closing. Lender requirements vary based on the property, state, project type, and construction stage.

A stronger file usually includes a clear budget, realistic timeline, experienced builder, documented borrower liquidity, completed plans, permit status, title information, valuation support, and a practical exit strategy.

Common delays include missing documents, unclear budgets, title issues, permit delays, insufficient liquidity, unrealistic completed value, unresolved zoning issues, incomplete contractor information, and weak exit strategy.

Many private lenders review credit, but requirements vary. Credit is usually considered along with collateral, liquidity, borrower experience, project budget, and exit strategy.

Foreign national investors may be eligible for certain business-purpose construction financing options, depending on documentation, entity structure, property location, collateral, liquidity, and lender/investor guidelines.

No. Submitting documents does not guarantee approval, funding, terms, or closing. All loans are subject to underwriting, borrower qualification, collateral review, valuation, state eligibility, and lender/investor guidelines.