Ground-Up Construction Financing

For Real Estate Investors

Ground-up construction financing helps real estate investors, builders, and developers fund new construction projects from land acquisition or land payoff through vertical construction and completion. Direct Private Capital Group, Inc. reviews land value, budget, plans, permits, borrower experience, LTC, LTV, ARV, draw schedule, liquidity, and exit strategy to help qualified borrowers explore private construction lending options. Terms vary and are subject to underwriting.

What This Page Helps Borrowers Understand

Ground-up construction financing is different from a simple purchase or refinance loan because the lender is reviewing both the current land value and the future completed project.

This page explains how private construction lenders may review land control, plans, permits, construction budget, borrower experience, loan-to-cost, loan-to-value, after-completion value, draw schedules, inspections, liquidity, and exit strategy.

A complete file does not guarantee approval or funding. It can, however, help Direct Private Capital Group, Inc. understand the transaction and review which available private lending options may fit the borrower, property type, state eligibility, project status, and lender/investor guidelines.

Who This Page Is For

This resource is designed for real estate investors, builders, developers, brokers, foreign national investors, commercial property owners, hospitality investors, gas station operators, and business-purpose borrowers seeking private real estate construction financing in the United States.

It may be useful when a borrower is building a new rental property, spec home, multifamily project, mixed-use property, commercial building, hotel project, gas station site, or other business-purpose real estate development.

Business-purpose financing note: Direct Private Capital Group, Inc. reviews business-purpose real estate financing scenarios. This page does not apply to consumer-purpose residential mortgage loans, owner-occupied consumer mortgages, or personal-purpose borrowing.

What Lenders Usually Review

Private construction lenders usually review land value, site control, plans, permits, construction budget, hard costs, soft costs, contingency, borrower experience, liquidity, draw schedule, inspections, loan-to-cost, loan-to-value, after-completion value, and exit strategy. Requirements vary by property type, state, borrower profile, project stage, and lender/investor guidelines.

What Can Delay Review

Common delays include missing plans, unclear permit status, incomplete budgets, no contingency line item, unsupported ARV, unresolved title issues, limited borrower liquidity, no draw schedule, contractor questions, expired approvals, environmental concerns, or a loan request that does not fit state or investor guidelines. Complete information can help the file be reviewed more clearly, but does not guarantee approval or funding.

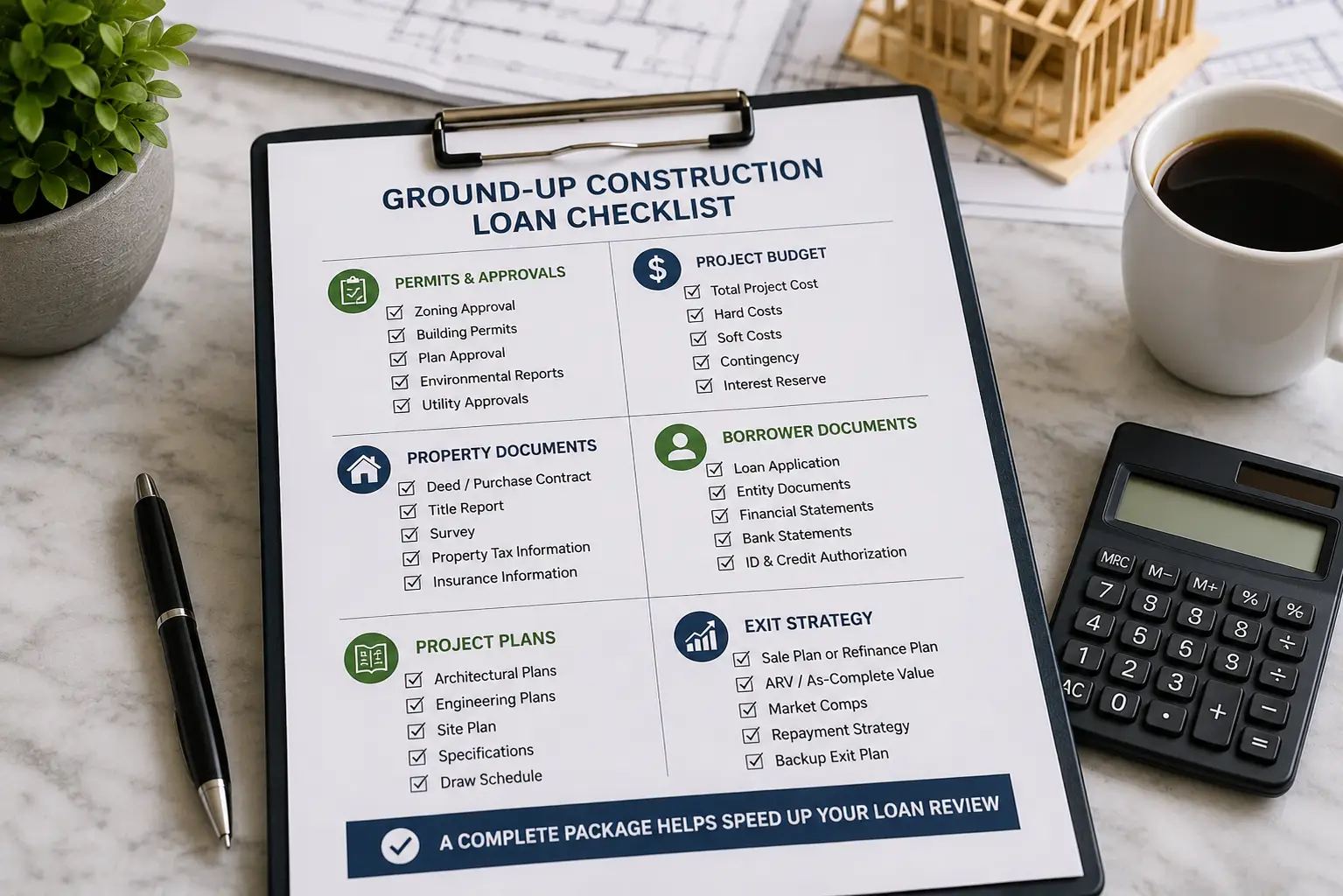

DOCUMENTS COMMONLY REQUESTED

BORROWER INFORMATION

- Borrower legal name, contact information, and borrowing entity

- Entity documents, ownership structure, EIN, and authorization to borrow

- Government ID, credit profile, liquidity, and proof of funds

- Builder/developer resume, prior projects, and construction experience

PROPERTY INFORMATION

- Property address, land size, proposed use, and current site condition

- Deed, purchase contract, title report, survey, payoff, and valuation support

- Plans, permits, zoning, entitlements, utility status, and site approvals

- Environmental reports or property-specific approvals when applicable

LOAN SCENARIO

- Requested loan amount, lien position, land payoff, and use of funds

- Construction budget, soft costs, contingency, interest reserve, and timeline

- Loan-to-cost, loan-to-value, after-completion value, and borrower contribution

- Draw schedule, exit strategy, repayment plan, and desired loan term

Submission note: Borrowers and brokers should confirm whether borrower documents, land ownership or site control, title information, plans, permits, construction budget, draw schedule, valuation support, liquidity, and exit strategy are available. Public resources from state contractor licensing boards, local building departments, and the U.S. Small Business Administration may provide general business or construction planning education. Loan review remains subject to underwriting, collateral review, state eligibility, and lender/investor guidelines.

GROUND-UP CONSTRUCTION LOAN REVIEW PROCESS

A clear submission helps Direct Private Capital Group, Inc. review whether available private lending options may fit the borrower, land value, construction budget, plans, permits, project timeline, draw schedule, after-completion value, exit strategy, state eligibility, and lender/investor guidelines.

FROM CONSTRUCTION SCENARIO SUBMISSION TO FUNDING CONSIDERATION

Preliminary review of land value, borrower profile, project status, plans, permits, requested loan amount, and exit strategy

Submit requested documents for underwriting, budget review, collateral review, valuation review, draw review, and title review

Closing conditions, title, insurance, valuation, draw controls, and funding consideration

Why Ground-Up Construction Financing Matters for Real Estate Investors

Ground-up construction financing matters because new construction projects often need capital before the property is completed, leased, sold, or refinanced. A borrower may control the land and have a realistic project, but still need private construction financing to move from plans and permits to completed improvements.

Private construction lenders usually want to understand whether the project can reasonably be completed, whether the budget is supported, whether the borrower or builder has relevant experience, and whether the completed property has a realistic sale or refinance exit.

A complete construction file does not guarantee approval or funding. It can make the review more efficient and help the lender or investor understand the land value, construction costs, borrower contribution, draw schedule, and repayment plan more clearly.

What Ground-Up Construction Financing Does and Does Not Mean

Ground-up construction financing may include review of land payoff, acquisition, hard construction costs, soft costs, contingency, interest reserve, and staged draws. It does not mean every project, borrower, budget, permit status, or property type will qualify.

It May Be Used For

- Spec home construction loans

- Build-to-rent investment projects

- Multifamily ground-up construction

- Mixed-use construction projects

- Commercial property development

- Hotel or hospitality construction

- Gas station or C-store site development

- Foreign national investor construction loans

- Business-purpose land payoff plus construction requests

It Does Not Mean

- No underwriting

- No collateral review

- No title review

- No valuation review

- No permit review

- No budget review

- Guaranteed approval

- Guaranteed funding

- Guaranteed rate or term

- Eligibility for every project in every state

Key Requirements, Documents, and Review Factors

Borrower Information Usually Reviewed

- Borrower name and contact information

- Borrowing entity name and entity documents

- Government-issued identification

- Credit profile, when required

- Real estate owned schedule

- Borrower liquidity and proof of funds

- Builder or developer resume

- Completed project history

- Personal financial statement, when required

- Foreign national documentation, when applicable

Property Information Usually Reviewed

- Property address, property type, land size, and proposed use

- Land purchase contract, deed, or proof of site control

- Current title report and existing liens

- Payoff statement if the land has existing debt

- Site plan, survey, plans, and specifications

- Zoning, entitlements, permits, and plan-check status

- Utility status and impact fees, when applicable

- Environmental reports for commercial, industrial, gas station, or specialized sites

- As-is land value and as-complete value support

Loan Scenario Information Usually Reviewed

- Requested loan amount

- Loan purpose

- Land cost or current land value

- Existing payoff, if applicable

- Total project cost

- Hard construction costs

- Soft costs

- Contingency

- Interest reserve request

- Borrower cash contribution

- Construction timeline

- Draw schedule

- Requested term

- Use of proceeds

Exit Strategy or Repayment Plan

The exit strategy explains how the borrower expects to repay the construction loan. Examples may include selling a completed spec home, selling completed units, refinancing into DSCR financing after lease-up, refinancing into permanent commercial debt, stabilizing a project and obtaining long-term financing, or repaying the loan from another documented capital source.

Loan Review Factors Table

| Review Factor | Why It Matters | What Borrowers Should Prepare |

|---|---|---|

| Land value | Shows the current collateral base before construction begins | Deed, purchase contract, appraisal, BPO, or valuation support |

| Loan-to-cost | Measures the loan amount against total project cost | Full development budget with hard costs, soft costs, contingency, and interest reserve |

| Loan-to-value | Measures the loan amount against current or completed value | As-is value and as-complete valuation support |

| ARV / as-complete value | Helps evaluate the completed project value | Appraisal, comps, broker opinion, or market support |

| Permit status | Shows whether the project is ready to begin | Permit card, approval letters, plan check status, or entitlement package |

| Borrower experience | Helps assess execution risk | Resume, completed projects, contractor background, and project team details |

| Liquidity | Helps cover overruns, interest, delays, and reserves | Bank statements, proof of funds, or financial statement |

| Draw schedule | Controls staged funding during construction | Line-item budget and draw plan tied to construction milestones |

| Exit strategy | Shows how the loan may be repaid | Sale plan, refinance plan, lease-up plan, or takeout plan |

Helpful construction planning note: Borrowers comparing financing structures may review general resources from local building departments, state contractor licensing boards, the U.S. Small Business Administration, and the U.S. Census Bureau. Private loan review still depends on the property, collateral, borrower profile, valuation, project status, loan purpose, state eligibility, and lender/investor guidelines.

Common Reasons a Ground-Up Construction Loan File Gets Delayed

- Missing construction budget

- Budget not broken down by hard costs and soft costs

- No contingency line item

- Unclear permit status

- Plans not approved or incomplete

- Expired entitlements or approvals

- Unclear land ownership or site control

- Title issues or unresolved liens

- Unsupported ARV or as-complete value

- Borrower liquidity not documented

- Contractor experience not provided

- No draw schedule

- No realistic construction timeline

- Exit strategy is vague

- Insurance requirements are not addressed

- Foreign national borrower documentation is incomplete

- Environmental concerns for commercial or gas station projects

How to Prepare Before Submitting a Loan Scenario

Prepare a Short Project Summary

- What is being built

- Where the property is located

- Who owns or controls the land

- How much the project costs

- How much loan proceeds are requested

- What stage the project is in

- When construction can begin

- How the loan will be repaid

Provide a Complete Budget

- Land cost

- Existing payoff

- Hard construction costs

- Soft costs

- Permits and fees

- Architecture and engineering

- Utility costs

- Insurance

- Interest reserve

- Contingency

- Developer contribution

Confirm Plans and Permits

- Fully permitted

- Permit-ready

- In plan check

- Entitled but not permitted

- Pending zoning approval

- Pending conditional use approval

- Still in design

Related Financing Topics

Ground-up construction financing may connect to hard money loans, bridge loans, DSCR loans, ground-up construction loans, commercial real estate loans, required documents, the loan process, FAQ, contact page, and apply now.

What This Page Does Not Guarantee

This page is educational. It does not guarantee loan approval, funding, terms, rates, closing timelines, search rankings, AI recommendations, or loan availability. Direct Private Capital Group, Inc. does not represent that every borrower, property, budget, permit status, or loan request will qualify for financing.

Loan availability may depend on borrower qualifications, credit profile, liquidity, collateral value, property condition, land value, construction budget, permit status, project team, draw structure, property type, loan purpose, loan amount, title condition, insurance availability, state eligibility, exit strategy, lender and investor guidelines, and applicable federal and state laws.

Submit Your Loan Scenario

If you are building a new residential, multifamily, mixed-use, commercial, hotel, gas station, or investment property, submit your ground-up construction financing scenario for review. Direct Private Capital Group, Inc. reviews business-purpose real estate construction loan scenarios across eligible U.S. markets.

Submit your loan scenario today and let Direct Private Capital Group, Inc. review available private lending options for your project.

Compliance Disclaimer

Direct Private Capital Group, Inc. provides business-purpose real estate financing information. This page is for informational purposes only and is not a commitment to lend, loan approval, or guarantee of terms. All loans are subject to underwriting, borrower qualification, collateral review, valuation, state eligibility, lender/investor guidelines, and applicable federal and state laws.

Helpful Construction and Business Resources

Borrowers may review general public resources from local building departments, state contractor licensing boards, the U.S. Small Business Administration, and the U.S. Census Bureau. Direct Private Capital Group, Inc. provides business-purpose real estate financing information, and this page is not legal, tax, valuation, construction, environmental, or consumer mortgage advice.Frequently Asked Questions About Ground-Up Construction Financing

Ground-up construction financing is a loan structure used to fund new construction projects, often including land payoff, construction costs, soft costs, interest reserve, and staged draws. Loan terms depend on underwriting, project details, collateral, borrower qualifications, and lender/investor guidelines.

Ground-up construction loans are commonly used by real estate investors, builders, developers, brokers, and business-purpose borrowers building new residential, multifamily, mixed-use, commercial, hospitality, or investment properties.

Common documents include a loan application, entity documents, borrower financials, ID, credit authorization, title report, plans, permits, construction budget, draw schedule, valuation support, borrower experience, proof of liquidity, and exit strategy.

Some private lenders may review land acquisition, land payoff, and construction costs together, depending on the land value, total project cost, requested loan amount, borrower contribution, permit status, and lender/investor guidelines.

Loan-to-cost compares the loan amount to the total project cost. Loan-to-value compares the loan amount to the property value, which may be based on as-is value or as-complete value depending on the lender’s review.

Usually, construction funds are released in stages through draws. Draws may require inspections, completed work verification, budget review, lien waivers, and lender approval before additional funds are released.

Not always, but permit status matters. A fully permitted or permit-ready project may be easier to evaluate than a project still waiting on zoning, entitlement, plan check, or conditional use approval.

Some private lenders may focus more on collateral, project value, liquidity, experience, and exit strategy than tax returns. Requirements vary by lender, loan program, property type, and borrower profile.

Common delays include missing plans, unclear permits, incomplete budgets, unsupported ARV, title issues, insufficient liquidity documentation, vague exit strategy, missing entity documents, or unresolved construction team questions.

No. Ground-up construction financing is not guaranteed. All loans are subject to underwriting, borrower qualification, collateral review, valuation, state eligibility, lender/investor guidelines, and applicable laws.