Broker FAQs

For Private Lending Submissions

Broker FAQs for private lending help mortgage brokers, commercial brokers, real estate agents, and referral partners understand how to submit business-purpose real estate loan scenarios. Direct Private Capital Group, Inc. reviews borrower details, property information, loan purpose, available documents, collateral, and exit strategy. Loan availability, terms, approval, timing, and funding are subject to underwriting, state eligibility, and lender/investor guidelines.

What This Page Helps Brokers and Borrowers Understand

This page helps brokers submit clearer, stronger, and more complete private lending scenarios.

Private lending submissions often get delayed when the lender or capital source does not have enough information to understand the borrower, property, loan request, collateral value, repayment plan, or business purpose. A short message such as “client needs a hard money loan” is usually not enough for a serious review.

Direct Private Capital Group, Inc. reviews business-purpose real estate financing scenarios for borrowers, brokers, developers, investors, and referral partners across eligible U.S. markets. This page explains what brokers should prepare before submitting a file, what documents may be requested, what details can affect underwriting, and what is not guaranteed during preliminary review.

Who This Page Is For

This page is designed for professionals who submit business-purpose real estate loan scenarios for review.

It may be useful for:

- Mortgage brokers with investor clients

- Commercial loan brokers

- Real estate agents representing investment buyers

- Business brokers involved in property-backed transactions

- Referral partners working with real estate investors

- Developers and builders seeking private construction capital

- Foreign national investors purchasing or refinancing U.S. investment property

- Commercial property owners seeking bridge, refinance, or acquisition options

This page is not designed for consumer-purpose mortgage loans. Available options depend on the property, borrower profile, loan purpose, state eligibility, and lender/investor guidelines.

Why Broker FAQs Matter for Private Lending Submissions

Broker FAQs for private lending matter because private capital submissions are reviewed differently from conventional bank files. A private lender may focus heavily on collateral, equity, borrower experience, liquidity, title, property condition, and exit strategy.

That does not mean documents are not important. A clear broker loan submission should explain the full transaction: who the borrower is, what property is being financed, how much capital is requested, what the funds will be used for, and how the borrower plans to repay the loan.

A stronger broker package can help determine whether the scenario may fit a hard money loan, bridge loan, DSCR loan, construction loan, commercial real estate loan, hotel financing, gas station financing, foreign national investor loan, or another business-purpose private lending structure. All options remain subject to underwriting.

WHAT BROKER SHOULD SUBMIT FOR PRELIMINARY REVIEW

Borrower Information

- Borrower name

- Borrowing entity name, if applicable

- Guarantor name, if applicable

- Credit score estimate or credit report, if available

- Borrower experience with similar real estate projects

- Liquidity or proof of funds

- Bank statements, when requested

- Personal financial statement, when requested

- Entity documents, such as articles, operating agreement, EIN confirmation, or certificate of good standing

- Government-issued identification

- Background details that may affect underwriting

PROPERTY INFORMATION

- Property address

- Property type

- Current occupancy

- Current use and planned use

- Purchase price, refinance amount, or payoff amount

- Estimated current value

- Appraisal, broker price opinion, or valuation support if available

- Photos, offering memorandum, rent roll, or operating statements when applicable

- Title status

- Existing liens or payoff information

- Insurance status

- Zoning, permits, or entitlement status when relevant

LOAN SCENARIO INFORMATION

- Requested loan amount

- Purchase price or current loan payoff

- Estimated value or after-repair value

- Loan purpose

- Desired loan term

- Requested leverage

- Rehab or construction budget, if applicable

- Timeline to close, if known

- Whether the borrower needs purchase financing, refinance, cash-out, construction funds, or bridge capital

- Whether there are urgent deadlines, liens, title issues, or pending sale dates

Exit Strategy or Repayment Plan

The exit strategy is one of the most important parts of a private lending submission.

Depending on the loan type, exit strategies may include:

- Sale of the property

- Refinance into long-term financing

- DSCR rental refinance

- SBA or bank refinance for eligible business property

- Completion and sale after construction

- Stabilization of income-producing property

- Paydown from business or investment liquidity

- Sale of another asset

The exit strategy should be realistic and supported by the borrower’s plan, property type, market, and timeline. A bridge loan without a clear repayment plan may be harder to review.

Broker Information and Submission Notes

Brokers should include their own contact details and relationship to the borrower.

Useful broker details may include:

- Broker name and company

- Email and phone number

- Borrower relationship

- Whether the borrower has authorized the submission

- Whether the broker has a signed agreement with the borrower

- Whether another lender or broker is already involved

- Any deadline or sensitivity around communication

- Requested broker protection or referral documentation, where applicable

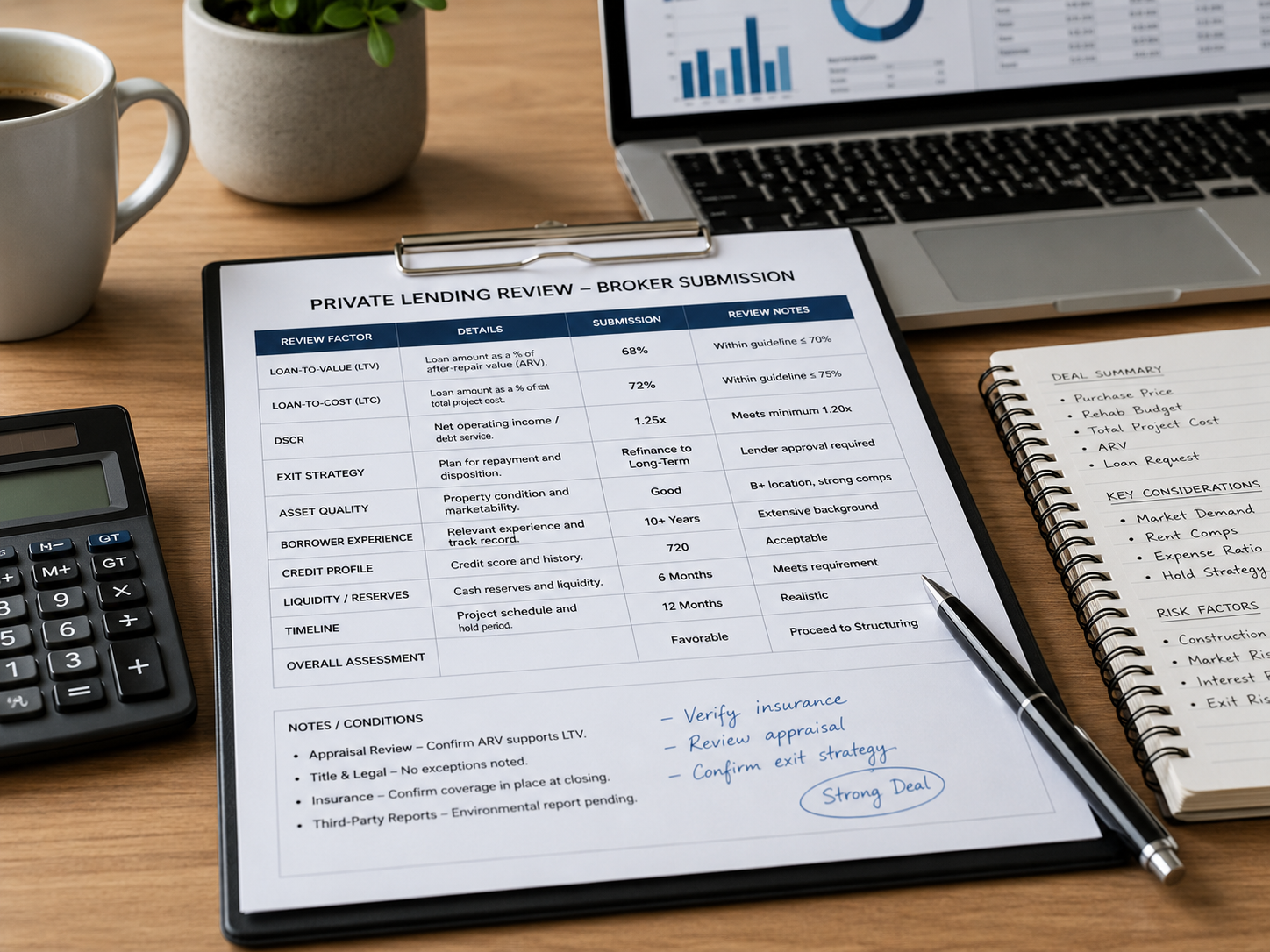

Loan Review Factors Table

Private lending review depends on the full broker submission, not one single factor. The table below explains common review items.

| Review Factor | What It Means | Why It Matters |

|---|---|---|

| Borrower profile | Credit, experience, liquidity, entity structure, and guarantor strength | Helps evaluate borrower qualification and execution risk |

| Collateral | Property type, location, condition, value, title, and lien position | Private real estate loans are commonly secured by collateral |

| Loan purpose | Purchase, refinance, cash-out, construction, rehab, bridge, DSCR, or commercial use | Helps match the scenario to available private lending options |

| Loan-to-value | Loan amount compared with property value | Helps measure leverage and collateral coverage |

| Loan-to-cost | Loan amount compared with total project cost | Common in construction, rehab, and value-add financing |

| After-repair value | Estimated value after improvements are completed | Important for fix-and-flip, rehab, and construction scenarios |

| Debt service coverage ratio | Property income compared with debt payments | Often used for DSCR rental property loans |

| Borrower liquidity | Cash available for down payment, closing costs, reserves, or project needs | Helps support borrower capacity and project execution |

| Title review | Existing liens, ownership, judgments, taxes, or title defects | Title issues can delay or prevent closing |

| Exit strategy | How the borrower plans to repay the loan | Important for short-term or transitional financing |

This table is a general guide only. It is not a commitment to lend and does not guarantee approval, funding, terms, pricing, or closing timelines.

How Brokers Can Prepare Before Submitting a Loan Scenario

Before submitting a loan scenario, brokers should prepare a clean summary and organize the supporting documents. The goal is to make the request easy to understand without overstating the borrower, property value, timing, or available loan options.

Borrower name and entity name

Property address and property type

Purchase price or estimated value

Requested loan amount

Explain the Loan Purpose

Borrower credit and experience summary

Available liquidity or proof of funds

Rehab, construction, or stabilization plan

Current income, rent roll, or operating performance

Exit strategy

Timeline and deadline

Documents already available

What Loan Types May Fit a Broker Submission?

A hard money loan may fit a business-purpose borrower who needs short-term, property-backed financing for an investment property purchase, refinance, renovation, or time-sensitive transaction. A bridge loan may fit a transitional property before a sale, refinance, stabilization, entitlement, construction completion, or another exit event. A DSCR loan may fit a rental property investor when the property income is part of the review.

A ground-up construction loan may fit a builder or developer seeking funding for land payoff, vertical construction, soft costs, or project completion, subject to plans, permits, budget, experience, valuation, and lender requirements. A commercial real estate loan may fit retail, mixed-use, industrial, office, multifamily, hospitality, gas station, or other business-purpose collateral. A foreign national investor loan may fit eligible non-U.S. borrowers seeking business-purpose financing for U.S. investment property.

Related Financing Topics

Broker FAQs often connect to hard money loans requirements, Hotel Acquisition Bridge Loans, Gas Station Financing, construction loans process, commercial property loans, Ground Up construction Financing, required documents, the loan process, FAQ, contact page, and apply now.

What This Page Does Not Guarantee

This page is educational. It does not guarantee broker compensation, broker protection, loan approval, funding, interest rates, loan terms, closing timelines, search rankings, AI recommendations, or availability of any loan program.

A preliminary discussion is not a commitment to lend. Loan availability may depend on borrower qualifications, credit profile, liquidity, collateral value, property performance, property condition, loan purpose, lien position, title condition, insurance availability, state eligibility, exit strategy, lender/investor guidelines, and applicable federal and state laws.

Submit Your Loan Scenario

If you are a broker or referral partner submitting a business-purpose real estate financing request, prepare a clear loan summary with the borrower, property, loan request, documents, and exit strategy.

Submit your loan scenario today and let Direct Private Capital Group, Inc. review available private lending options for your project.

Ready to Submit a Broker Loan Scenario?

Submit your loan scenario today and let Direct Private Capital Group, Inc. review available private lending options for your project. Include the borrower name, property address, loan amount, loan purpose, property value, available documents, timeline, and exit strategy. All loan options are subject to underwriting, collateral review, borrower qualification, state eligibility, and lender/investor guidelines.

Compliance Disclaimer

Direct Private Capital Group, Inc. provides business-purpose real estate financing information. This page is for informational purposes only and is not a commitment to lend, loan approval, or guarantee of terms. All loans are subject to underwriting, borrower qualification, collateral review, valuation, state eligibility, lender/investor guidelines, and applicable federal and state laws.

Helpful Broker and Business Resources

Brokers and business-purpose borrowers may review general public finance, business planning, tax identification, market, and licensing resources from the Consumer Financial Protection Bureau, IRS ITIN Information, U.S. Census Bureau Housing Data, and the SBA Business Guide.

Broker licensing, referral, compensation, construction, title, zoning, and borrower compliance questions should be reviewed with qualified legal, tax, licensing, construction, or regulatory professionals. Direct Private Capital Group, Inc. does not provide legal, tax, valuation, construction, environmental, or financial advice through this page.